What a pilot delivers

Sample report: Single Mega Winner case

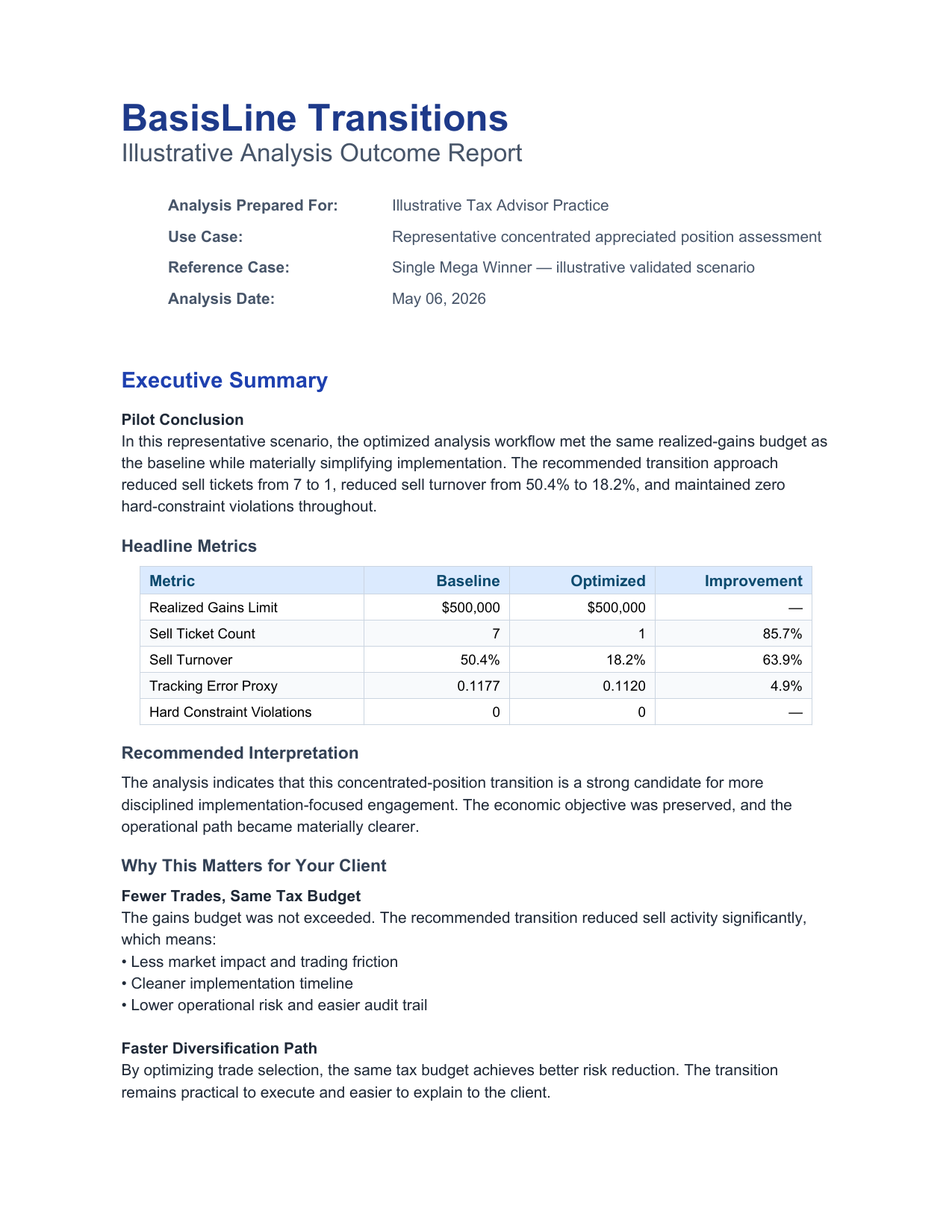

The lead example is a large single appreciated position under a $500K realized-gains budget transitioning into a benchmark-aware custom indexed portfolio. The sell ticket reduction concentrated position metric is one of the primary outputs.

Illustrative pilot outcome pack

Representative example deliverable — structure and depth of a completed pilot engagement.